Case Study: Atour Lifestyle (ATAT)

A deep-dive case study on Atour Lifestyle Holdings (NASDAQ: ATAT), the Chinese hotel chain reinventing itself as a hybrid retail platform. Explore how Atour turns hotel rooms into showrooms, scales culture through its ‘commissar’ system, and challenges traditional hospitality models

SPAWNERSTRAVELHOTEL GROUPS

lee kelsall

8 min read

Overview

In 2013, at the height of China’s urban consumption boom, a small group of hoteliers and brand-builders set out to answer a simple question: could a domestic chain deliver the design, service, and cultural cachet of a global lifestyle brand—without copying a foreign playbook?

A decade on, Atour Lifestyle Holdings (NASDAQ: ATAT) has emerged as one of China’s most distinctive midscale hotel operators, known for curating every sensory detail—from the scent in its lobbies to the soundtrack in its rooms.

But Atour is no longer just a hospitality company. It is a founder-led, vertically integrated lifestyle platform that straddles hospitality and consumer goods—leveraging its 1,700 hotels as a national showroom and distribution network for its growing retail portfolio. This dual identity makes Atour an intriguing proposition, and perhaps a blueprint for other global hotel groups seeking to build a harmonised digital–physical ecosystem at the intersection of travel, wellness, and retail.

There is, however, a catch. The stock has more than doubled over the past year as investors have recognised the shift in narrative. At today’s forward Price/FCF multiple of ~18x—around 50% higher than its nearest domestic peer, H World—valuation is a sticking point. Yet the comparison is imperfect: H World’s scale, brand portfolio, and international footprint differ materially, and none of its peers replicate Atour’s integrated retail engine, which is now a key driver of both revenue and earnings growth.

The real question is how Atour should be valued: as a fast-growth retail brand with scalable distribution, deserving a consumer-brand multiple in the mid-to-high 20s; as a capex-light, manachised hotel operator, typically valued in the low teens; or as something in between — a hybrid platform where the retail flywheel justifies a structural premium over traditional hotel peers while the hotel base provides defensive cash flow. The market today appears to be pricing it somewhere in the middle. Whether that gap closes toward retail valuations or reverts toward hotel comps will hinge on the scale and defensibility of Atour’s retail ecosystem.

A Curious Line in the Financials

And now we arrive at the BOOM! moment.

Buried in the financials is a line called “sales of hotel supplies and other products.” In FY2024, it clocked in at RMB 2.0 billion. That’s not guest shampoo bottles or lobby trinkets. That’s Atour selling its branded products wholesale to franchisees.

Here’s the play:

Atour supplies pillows, sheets, toiletries, and furniture to manachised hotels at a wholesale discount (likely 25–30% below retail).

Franchisees resell to guests under Atour’s pricing guidance, keeping the margin.

Guests get a seamless, standardised experience — and often take the products home.

In other words, every new hotel opening generates not just franchise fees, but also a large procurement order. Atour monetises its design ethos twice: once through the stay, and again through the supply chain.

Add up direct retail sales + wholesale supply sales, and you suddenly see the real picture: the combined retail/supply engine is the single largest revenue driver in the company. Larger than room revenue. Larger than franchise fees.

Atour isn’t just a hotel group. It’s a retail distribution network disguised as one.

Strategic Positioning

Atour focuses on China’s expanding middle-class traveller—particularly Gen Y and Gen Z urban professionals who seek lifestyle-oriented, personalised hospitality. Positioned above budget chains but below luxury, Atour avoids price wars and luxury overcapacity, while targeting a segment underpenetrated by international brands.

The company’s “Warmth Aesthetics” ethos blends boutique individuality with the reliability of a scaled chain. Sensory marketing—from signature scents to curated playlists—supports a Peak–End design principle, embedding positive emotional peaks and final impressions in guest memory.

Atour’s proprietary technology stack—CRS, PMS, CRM, and MRPS—integrates hotel operations with retail distribution:

AI-driven demand forecasting & pricing.

Centralised procurement of hotel/retail SKUs, ensuring consistency and scale benefits.

Unified guest profiles linking room stays and retail activity.

Reduced OTA dependency via direct bookings and retail integration.

This infrastructure allows Atour to run a capital-light franchising model while layering on retail distribution through its hotel footprint.

~97% of Atour’s rooms operate under the manachise model, where franchisees fund CapEx and leases, while Atour provides managers, systems, and brand oversight. Contracts run 8–15 years with upfront fees, monthly royalties, and mandatory supply purchases. Compared with peers, Atour derives a higher share of revenue from franchising (~80% vs. 25–49% for competitors), yielding stable, asset-light earnings.

Atour rooms cost ~RMB 140k to build—slightly higher than peers—but deliver 3–5 year payback thanks to stronger RevPAR. Mid-life renovations pay back in ~3 years. Franchisee selection is strict, often repeat operators, ensuring network quality and profitability.

Atour’s A-Card loyalty program (88M members, 53% of room nights by 2023) is central to customer retention. It not only drives higher booking frequency and direct traffic but also increases retail purchase attach rates. Tiered benefits (late checkout, early access, exclusive rates) enhance brand attachment, reducing OTA dependence.

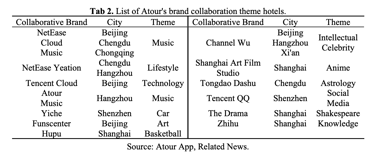

Atour blends hospitality with cultural resonance. Its IP-themed hotels—developed with partners like NetEase Cloud Music and Shanghai Arts Film Studio—immerse guests in nostalgic, culturally rich environments, generating memorable “peak moments” that resonate with younger consumers. This IP strategy mirrors Disney’s hotel + people + IP formula, deepening emotional loyalty and broadening Atour’s reach.

The Opportunity

When Atour launched in 2013, the budget and luxury segments of China’s hotel market were already crowded. BTG Homeinns and Jin Jiang had consolidated the low end, while Marriott, Hilton, and Accor dominated the five-star tier. The mid-to-high-end space — essentially the four-star equivalent — remained underserved by domestic brands offering a design-led, lifestyle-oriented experience. This gap coincided with the rapid expansion of China’s middle class and a willingness to pay for comfort, aesthetics, and perceived quality. Atour’s early bet on this segment allowed it to scale without head-to-head pricing wars in the budget tier or the capital-intensive demands of true luxury.

Today Atour Lifestyle Holdings (NASDAQ: ATAT) operates over 1,700+ hotels across China under an asset-light, manachised model (management contract with the option to convert to a franchise contract), with an usually fast growing strong consumer retail brand extension. It’s a company that invites closer scrutiny—especially for anyone with operational experience in hospitality.

Atour boasts six accommodation brands: A.T. House, Atour S Hotel, Atour (Flagship) Hotel, Atour X, Atour LIGHT, and its newest upscale hotel brand SAVHE covering mid-range, mid-to-high-end, high end, and luxury segments. Starting from hospitality, the company has since expandinto scenario-based lifestyle retail. It developed two major retail brands, "ATOURPLANET," covering sleep-related products, including pillows and comforters and "SAVHE," ”a private label line that targets personal care and fragrance, including shampoo, handwash and diffusers.

Management & Culture

Founded in 2013, Atour (亚朵) takes its name from a small Yunnan village on the China–Myanmar border, a place defined by simplicity, harmony, and spiritual well-being. This symbolism anchors Atour’s philosophy of creating scenes that convey warmth and beauty. More than hotels, Atour aspires to cultivate genuine human connection through design, service, and sensory experience.

Atour has been founder-led since inception. CEO Wang Haijun, a veteran of H World, retains a significant ownership stake (>30%), aligning management incentives with long-term brand development. This insider alignment underpins Atour’s discipline in maintaining design quality, customer satisfaction, and consistent brand execution.

A hallmark of Atour’s culture is embedding service design into daily operations. Each property integrates 16+ service touchpoints and the unique “Commissar” role—a franchisee-funded but Atour-trained manager responsible for HR, training, and cultural alignment across the network. This ensures the delivery of Atour’s lifestyle ethos at scale.

In contrast to China’s historically rigid service culture, Atour empowers front-line employees with discretion and budget to solve guest problems in real time—from purchasing medicine to accompanying guests to hospitals. Complaints must be addressed within the same day, with managers submitting rectification plans reviewed centrally. Guests are invited to “scan and complain” (扫码吐槽 必有回响), signalling Atour’s confidence in responsive service.

Atour leverages proprietary CRS/PMS/CRM systems to log guest preferences and deliver tailored experiences—down to pillow choice, scent, lighting, and curated in-room playlists. Signature touches like pillow menus, scent branding, and locally sourced amenities both differentiate the stay and feed into Scenario-Based Retail, allowing guests to purchase Atour products for home. This sensory, tech-enabled loop deepens loyalty and drives repeat business.

If you’ve worked with Atour—or have insight into its supply chain, franchising model, or retail structure—I’d love to connect.

Disclaimer:

The content published on this site is for informational and discussion purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities. The author may hold positions in the securities or companies discussed and may change these positions at any time without notice. All views expressed are personal opinions and should not be relied upon for investment decisions. Do your own research.

Scenario Based Retail

Here’s where it starts to gets interesting. Atour has built what is arguably China’s first digitally native retail arm within a hotel chain. Rather than treating retail as an afterthought, the company wove it directly into the guest experience. The focus is sleep — not just beds and pillows, but the entire ecosystem of comfort. Through its Atour Planet line, the company designs pillows, comforters, and other products that aim to transform sleep from a basic need into a restorative experience. Its second line, SAVHE, extends into personal care and fragrance — shampoos, handwash, diffusers — reinforcing the sense of wellness that begins in the room and lingers at home. Guests encounter these products in lobbies, rooms, and through the A-PLUS service, where they can trial items during their stay and buy them instantly through Atour’s mobile app, Weixin mini-program, or major e-commerce platforms. Today, nearly 90% of retail revenue is generated online, with delivery just a few taps away.

Behind the scenes, Atour runs a disciplined market research and supply chain engine. It surveys customers, identifies emerging trends, designs products, and partners with third-party manufacturers under strict quality protocols — samples tested in-house, random spot checks, compliance with national standards. This lean but controlled supply chain has enabled Atour to scale quickly while maintaining quality. By 2024, the retail segment reached RMB 2.59 billion in GMV, and management sees the sleep category as only the starting point. The ambition is to expand into adjacent “sleep scenarios” while creating incremental value for franchisees, who resell Atour products in their hotels under company pricing guidance. In other words, Atour’s hotels are not just places to stay; they are distribution nodes in a national lifestyle brand experiment.

Valuation

On valuation, I’ve kept things deliberately rough and ready — essentially reverse-engineering Atour’s two main divisions (hotels vs. retail/supply chain) from the footnotes.

To get to ballpark profits, I split shared costs like sales & marketing and technology 50/50 between the two. On that basis, the hotel arm generated just under RMB 1.0 billion of operating profit in 2024, which, at a 12–14× peer multiple for franchised hotel groups, suggests a value of RMB 12–14 billion.

The retail and supply chain side produced around RMB 560 million of operating profit; applying a consumer brand-style multiple of 20–25× gives another RMB 11–14 billion.

Together that implies RMB 23–28 billion (US$3.2–3.9 billion) of equity value.

At today's share price of US$33/share (about 10% above my entry level), Atour’s current market cap of about US$4.3 billion (RMB ~31 billion) therefore looks like a blended premium — pricing the company somewhere between a straight hotel chain and a consumer brand.

Interestingly, on my math, retail and supply chain now account for nearly 60% of revenues, which goes some way to explaining why investors are willing to stretch beyond hotel-peer multiples.

Whether that premium looks justified will hinge on how far retail margins can scale from here but if the market does buy the retail narrative (my hunch) then we could see further multiple expansion from here.

Copyright Komorebi Investments Pty Ltd 2025