Case Study: Fountaine Pajot (ALFPC)

Fountaine Pajot (EPA: ALFPC) deep dive case study: a decades-old, family-owned catamaran builder listed in Paris, combining strong cash flow, ODSea Lab electrification, and vertical integration to capture long-term growth in the global yacht market.

SPAWNERSTRAVELELECTRIFICATION

lee kelsall

12 min read

History of Fountaine Pajot (ALFPC)

In 1976, on the windy Atlantic coast of France, two young sailors—Jean-François Fountaine and Yves Pajot—decided to turn their racing pedigree into something bigger. From a modest boatyard in La Rochelle, they began building catamarans that married performance with French design flair. What started as a passion project for competitors at sea became a brand that carried French sailing culture across oceans.

Nearly fifty years on, Fountaine Pajot still feels like that original workshop: entrepreneurial, independent, family-run. But the scale has changed. Listed on Euronext Paris under the ticker ALFPC, the company is now a €160 million microcap and the second-largest series-production leisure boatbuilder in Europe (behind Group Bénéteau). It generates steady cash, remains tightly owner-operated, and through its ODSea Lab initiative is pushing into marine electrification and vertical integration. It also sits on a cash balance amounting to roughly 70% of its market capitalisation—an unusual profile in today’s market, and one that makes it worth dissecting closely.

Whilst yacht manufacturing is not my core domain, a decade spent building a luxury safari operator—marketing high-ticket products to HNWIs and UHNWIs through multiple market cycles—gives me an adjacent lens on the strategies that can propel a brand at the intersection of design, lifestyle, and experiential luxury.

Disclaimer:

The content published on this site is for informational and discussion purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities. The author may hold positions in the securities or companies discussed and may change these positions at any time without notice. All views expressed are personal opinions and should not be relied upon for investment decisions. Do your own research.

Management & Culture

Fountaine Pajot is led by Nicolas Gardies, a measured operator with over two decades at the company, supported by a highly aligned leadership team that includes Romain Motteau and Mathieu Fountaine, ensuring continuity with the founding family. Insider ownership stands at 54%, concentrated among family members and long-serving employees — reinforcing a culture of stability and long-term stewardship.

From peers, former employees, and industry voices, the company is often described as very “French”: pragmatic, discreet, and quality-driven, but historically less outward-facing. This cultural identity has underpinned its reputation for craftsmanship and reliability, yet has arguably limited its commercial reach outside France — evident in modest international sales penetration relative to competitors, low-key shareholder communications, and minimal analyst coverage.

From its origins with just four staff, Fountaine Pajot has grown into a team of more than 1,200 collaborators across three specialized sites: Aigrefeuille (core sailing catamarans), Port Neuf, La Rochelle (flagship catamarans with direct-launch facilities), and Gujan-Mestras (motor yachts). This blend of insider alignment, generational continuity, and industrial focus supports a culture built for endurance rather than spectacle — a defining characteristic in an industry prone to cyclical swings and passing fashions.

Strategic Positioning

Over the past five years, Fountaine Pajot has made a series of deliberate strategic moves that reveal an ambition far greater than first impressions might suggest. The company has diversified its offering both within the catamaran segment and beyond — most notably through the acquisition of Dufour — with a targeted focus on higher-value, premium segments. Its rebrand positions the company more firmly in the luxury space, framing its products as timeless, crafted, and artisanal — evoking the heritage of Swiss watchmaking or French luxury goods. At the same time, Fountaine Pajot has doubled down on its market-leading stance in electrification and taken greater control of its value chain, moving upstream via acquisitions of key sales distributors and downstream through the purchase of its interior manufacturing partner.

Electrifying the Blue Economy

Marine electrification remains technically complex. Boats are weight-sensitive, require long range, and operate in harsh, variable environments—factors that make battery integration and hybrid propulsion less straightforward than in cars. Today, most leading yacht manufacturers—especially in the superyacht category—offer hybrid or electric models, including Sanlorenzo, Azimut-Benetti, and Silent Yachts. In the catamaran space, players like Catana and Groupe Bénéteau (through its Excess and Lagoon brands) have also introduced hybrid-ready vessels, often in collaboration with third-party propulsion suppliers. At the same time, a wave of sustainability-first newcomers is expanding the competitive set. Builders like Vaan Yachts, with its recycled-aluminium hulls, MODX, pursuing fully electric and ultimately autonomous systems, and Silent Yachts, pioneering 100% solar propulsion, are drawing in a fresh cohort of customers—whether charterers or first-time owners—whose entry point to boating is defined as much by environmental values as by performance or design.

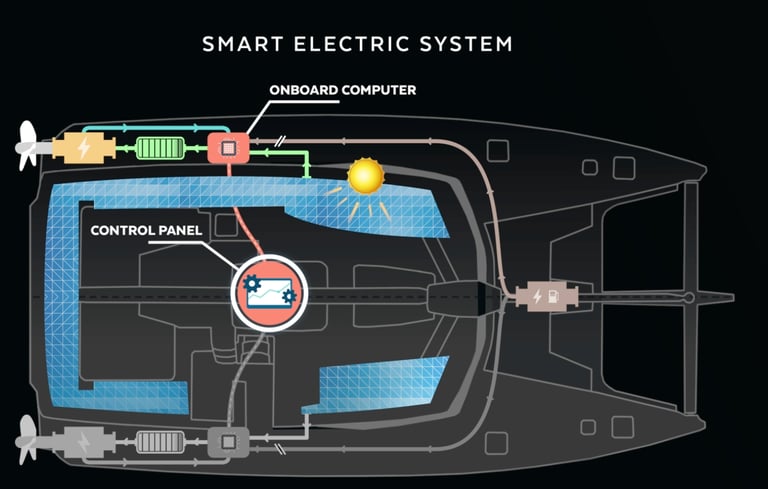

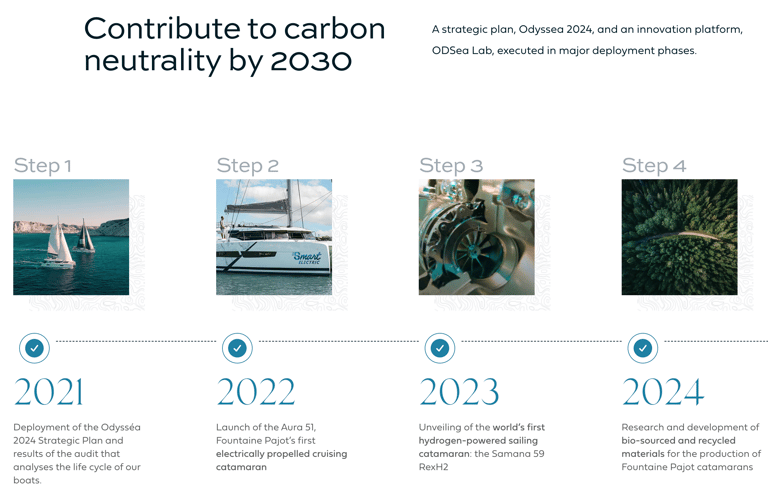

Fountaine Pajot is pursuing a more integrated approach. Through its ODSea+ initiative and the 2022 acquisition of Alternative Energies, the company has brought key electrification capabilities—solar, battery, and propulsion system design—in-house. Since 2021, it has introduced over 30 hybrid or electric boats, including models featuring 2.3kW solar arrays and a proprietary 25kW hybrid system developed by its ODSea Lab.

Fountaine Pajot’s Aura 51 Smart Electric model is already in series production, and the Samana 59 Smart Electric REXH2 prototype pushes further—integrating hydrogen-powered, zero-emission propulsion via the REXH2 fuel cell system that harnesses solar, lithium battery storage, and hydrogen to deliver extended autonomy at sea. Through ODSeaLab, and with over 60 engineers collaborating under the Odysséa 2024 strategy, the company is embedding sustainability right at the core of design, production, and lifecycle—from energy innovation to zero-carbon operation.

While Fountaine Pajot is not alone in electrification, its decision to control more of the value chain—rather than relying solely on outside vendors—suggests a longer-term commitment to building differentiated systems and product platforms across its multihull range.

Valuation

Despite its progress, we believe Fountaine Pajot remains deeply undervalued if you take a 3-5 year view.

At the end of FY2024 the company had €66 million of net free cash on the balance sheet. With ~€20 million earmarked for new model development, that still leaves ~€46 million available for distribution over time.

Valuation:

Share Price: ~€104 (52 week high: ~€120, 52 week low: ~€80)

Market Cap: ~€180m

Cash: €66m

LT Debt: €25m

EV: ~€139m

Profitability & Multiples (TTM):

NOPAT: €33m

EV/NOPAT: ~4x

EV/Sales: <0.4x

P/E: <6x

Price/Book: ~1.5x

Stormy Seas Ahead

The competitive landscape in 2025 highlights both resilience and fragility across Europe’s listed yacht builders. Sanlorenzo continues to set the benchmark, with revenues and margins still growing, but management has struck a more cautious tone on the outlook given global uncertainties, even as its ultra-high-net-worth positioning keeps order books strong. The Italian Sea Group, meanwhile, saw profits contract sharply and leverage rise, with the added overhang of reputational risk from the ongoing Bayesian disaster investigation — a potential headwind for forward sales in its core superyacht segment. Among the smaller and mid-sized players, Fountaine Pajot stands out as the most disciplined: revenues dipped modestly but profitability actually improved, backed by a net cash fortress, premium product mix, and continued reinvestment in electrification and vertical integration. By contrast, Catana’s sales retreated sharply and margins eroded, exposing its vulnerability to down-cycle demand swings, while Bénéteau remains weighed by its scale exposure to mass-market volumes despite its balance sheet strength. Taken together, FP emerges as the best positioned of the small-to-mid-cap builders — a company compounding quietly while peers either struggle for footing or face reputational and cyclical headwinds.

Against this backdrop, Fountaine Pajot stands out. Unlike peers that rely heavily on subsidised charter fleets or price discounting, FP enters this down-cycle with record profitability, a net cash fortress, and an owner-operator culture that has historically avoided chasing volume at the expense of margins. Its ODSea Lab electrification program and push into larger, higher-margin multihulls position it closer to the Sanlorenzo playbook than to mass-market peers. Yet at ~4x EV/NOPAT that disconnect is precisely where the opportunity lies. By comparision Sanlorenzo is trading on ~12x EV/NOPAT and whilst we acknowledge the difference in positioning and pedigree, we do not think that differencial is warranted.

We estimate that FP generated around ~€50m in FCF before NWC movements in 2024. Assuming it can get back to something similar by August 2027 then we think a ~€400 million market cap is not out of question. That would be a nice 2.5x from today’s depressed prices.

Risks

The key (short term) downside risks are:

A prolonged post-COVID demand correction

Tariff exposure

Pullback in discretionary yacht spending by HNWIs

A slowing secondary market creating pricing pressure

Variant View

Where the market sees a French boatbuilder in a cyclical niche, navigating tariff noise and post-COVID normalization, we see a disciplined, family-run business positioning itself for the next decade. Fountaine Pajot has weathered cycles before, and while short-term sales may soften, its reinvestment in new models, careful capital allocation, and ODSea Lab electrification program point to a company steadily strengthening its hand. In a fragmented global industry, that combination of owner-operator culture and vertical integration is quietly building a moat before the market recognises it.

Final Word

Fountaine Pajot is not without risk. Leisure boats remain discretionary, and tariffs, FX swings, or a global slowdown could dent demand. But with robust free cash flow, deep insider alignment, and a measured long-term vision, the downside looks contained. The opportunity, meanwhile, is understated: the brands that will win the next cycle are those able to electrify, verticalise, and globalise. Fountaine Pajot is taking each of those steps—quietly, deliberately, and with a time horizon that extends beyond the storm.

One additional lever remains underutilised: engaging the capital markets more proactively. Despite delivering Ferrari-like returns on capital, the company trades closer to a cyclical industrial, largely because it has kept a low profile with investors. By enhancing shareholder communications, providing clearer disclosure, and hosting targeted investor events, Fountaine Pajot could broaden its investor base, lower its cost of capital, and close the valuation gap with peers such as Sanlorenzo. In doing so, it would not only raise its profile with the financial community, but also reinforce global brand equity with clients, distributors, and employees.

For a business already compounding quietly, this is an open goal: low cost, low risk, and high potential reward.

The Opportunity

Fountaine Pajot designs and manufactures luxury catamarans — both sailing and power — as well as monohull yachts under two brands: its eponymous multihull line and Dufour Yachts, acquired in 2018. Since its founding, the group has launched more than 14,500 vessels worldwide and today operates at the top tier of the global multihull market.

In sailing catamarans, Fountaine Pajot is one of the leading producers alongside fellow French groups Bénéteau (Lagoon and Excess), Catana Group (Bali), Sunreef, and South Africa’s Robertson and Caine (Leopard). Together, these builders dominate an estimated 65–70% of worldwide sales, with Fountaine Pajot maintaining a 10–12% global share in this segment — a meaningful position in one of the most competitive categories in leisure yachting.

The company is also carving out a position in the faster-growing Power Catamaran market through its dedicated Motor Yacht range (MY4S, MY5, MY6, Power 67). Globally, power cats now represent nearly 60% of catamaran market value, equivalent to about USD 1.3 billion in 2025 and projected to grow further to USD 1.7+ billion by 2030. Fountaine Pajot’s Motor Yacht revenues are estimated at €40–55 million (~USD 45–60 million), giving it a 3–5% global share — smaller than in sailing, but with higher long-term upside given strong demand growth in North America and Southeast Asia.

Over the past four years, the group has executed its ODYSSEA 2024 plan, nearly doubling revenues from €172 million in 2020 to €351 million in 2024, without shareholder dilution — funding expansion through internal cash flow and disciplined reinvestment. Growth has been underpinned by international diversification (Europe ~50%, North America ~30%, Asia-Pacific ~20%), integration of supply chains (bringing electric propulsion and carpentry in-house), and innovation in sustainability. Fountaine Pajot has already launched more than 30 hybrid or electric-powered boats, and through its ODSeaLab initiative and acquisition of Alternative Energies, is building proprietary expertise in solar, battery, and propulsion systems. At the same time, the group has established the Nautical Talent Institute to deepen the skills pipeline needed to sustain its growth.

Globally, catamarans have grown at a 7%+ CAGR since 2019, significantly outpacing monohull yachts, particularly in the 40–60 foot leisure segment. Their appeal is clear: greater stability, wide deck and living space, and shallower draft make them ideal for family cruising, charter fleets, and new sailors prioritizing comfort and safety over pure speed. Catamarans are especially well-suited to American coastal cruising and intracoastal waterways, yet they remain underpenetrated in the U.S. despite the country representing nearly half of global boating revenues. This underrepresentation, coupled with growing adoption among anglers, day cruisers, and charter operators, points to a significant runway for further growth — particularly in power catamarans, where Fountaine Pajot has begun to position itself for leadership.

ODYSSEA 2028: A Blueprint for Growth

Looking ahead, Fountaine Pajot has laid out a clear five-year roadmap. Under its ODYSSEA 2028 plan, the group will launch 11 new models (6 catamarans, 5 monohulls), continue its electrification push, and invest €19 million into modernising production.

A particularly strategic product is the upcoming Code 07—a 50-foot motor yacht designed specifically for U.S. buyers. Developed under the Veya brand—a joint venture between Fountaine Pajot and French builder Couach Yachts—the Code 07 represents Fountaine Pajot’s boldest effort yet to enter the U.S. power yacht market.

This JV is being led by Romain Motteau, the company’s Deputy Managing Director, signaling the seriousness of the initiative. If successful, it could unlock a large, brand-loyal customer base—and expand margins beyond the European sailing crowd.

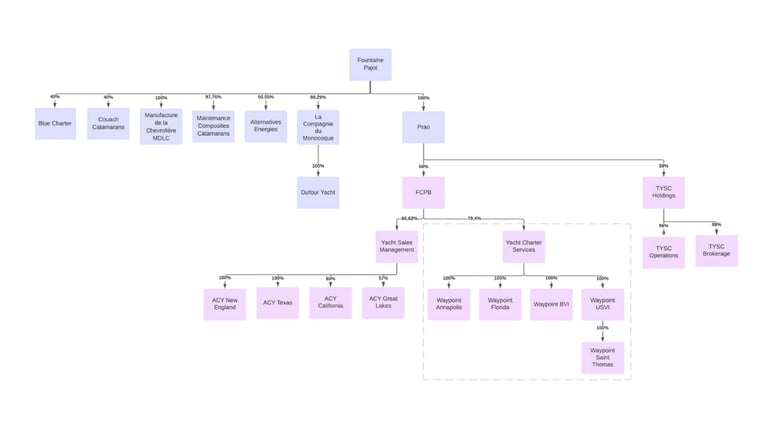

Vertical Integration: Owning the Journey

But electrification is only one part of the transformation. The company is bringing the value chain in-house. To reduce dependency on suppliers and elevate the brand experience, Fountaine Pajot has been following the lead of listed superyacht peers SanLorenzo and The Italian Sea Group by vertically integrating both its supply chain and sales funnel:

In 2024, it acquired Malvaux Industries’ 8,000 m² outfitting plant in La Chevrolière, giving it greater control over cabinetry, interiors, and finishings.

In the same year, it took a controlling stake in The Yacht Sales Co., a premier distributor in Asia-Pacific with presence in 11 countries—boosting both sales reach and customer service. This follows on from the 25% stake it acquired in Atlantic Cruising Yacht, a US based distributor, in 2023.

In 2022, it acquired Alternative Energies, bringing electric propulsion and hybrid R&D into the group.

This approach mirrors the best compounders in other industries: control the brand, own the engineering, deepen customer relationships, and scale quality.

Luxury-Like Economics Without the Luxury Overhead

What stands out from a peer-to-peer review of the last twenty years is that Fountaine Pajot’s financial profile has quietly converged with the Italian super-yacht builders. Since 2018, the group has consistently delivered gross margins above 50% and normalised ROIC in the 15–28% range—levels broadly comparable to Sanlorenzo and The Italian Sea Group. Yet unlike those peers, Fountaine Pajot operates with a leaner cost structure. Where Sanlorenzo and TISG absorb much of their extraordinary 60–80% gross margin into SG&A to maintain the aura of ultra-luxury brands, Fountaine Pajot spends far less on brand theatre, and more of its gross margin flows through to EBIT. The result is a company that achieves luxury-adjacent returns with a mid-market brand perception.

A Mispriced Niche Compounder?

This raises an intriguing investment angle. Public markets often categorise Fountaine Pajot alongside industrial boatbuilders such as Groupe Bénéteau and Catana Group, whose long-term returns on capital rarely exceed single digits. But the evidence suggests Fountaine Pajot is structurally different: a capital-light semi-custom model financed by deposits, resilient mid-cycle margins, and returns on capital closer to a Ferrari-style yacht builder than a mass-market manufacturer. If the market continues to value FP like a cyclical industrial while it delivers returns more akin to a proto-luxury compounder, investors may be looking at a mispriced asset hiding in plain sight.

Lessons From Luxury: How Scarcity Creates Moats

From my years inside the luxury end of the safari industry, I learned that value wasn’t always correlated with the quality of the lodge location, but in the perceived quality of the brand via brand storytelling. Brands like Singita, Wilderness, &Beyond and Asilia managed to secure prime locations in the best reserves but they were far from alone. Their strength lay in building strong brand recognition for quality and luxury, through aggressive expansion into complimentary locations, combining those locations through logistics and vertically integrating the ground-handling and direct sales functions. Perceived scarcity, brand, and distribution combined to create moats far larger than the sum of their parts.

Catamarans share many of these structural traits. It is a niche segment of the market (albeit Power catamarans are growing in popularity). There are a handful of builders who have the production capacity to build more than 100 vessels annually. Yard capacity naturally limits supply for the smaller operators; and is fragmented between a long tail of custom builders. This is creating a similar emerging oligopoly of scaled players; and the product, like a safari, is as much about identity and storytelling as it is about utility. Here, too, the advantage will accrue to those who lean into brand, vertical integration, and control of distribution.

For Fountaine Pajot, the path forward is not simply producing more units, but consolidating its positioning as a trusted luxury brand with direct reach to customers — occupying the strategic space where scarcity, heritage, and distribution power converge. Its consistent improvement in Gross Margin % would indicate it has subtly improved its pricing power either through operational efficiencies or passing through cost increase+ to customers.

Copyright Komorebi Investments Pty Ltd 2025