Fountaine Pajot (ALFPC) investment thesis

Fountaine Pajot (EPA: ALFPC) stock analysis: a decades-old, family-owned catamaran builder listed in Paris, combining strong cash flow, ODSea Lab electrification, and vertical integration to capture long-term growth in the global yacht market.

SPAWNERSTRAVELELECTRIFICATION

lee kelsall

8 min read

History of Fountaine Pajot (ALFPC)

In 1976, on the windy Atlantic coast of France, two young sailors—Jean-François Fountaine and Yves Pajot—decided to turn their racing pedigree into something bigger. From a modest boatyard in La Rochelle, they began building catamarans that married performance with French design flair. What started as a passion project for competitors at sea became a brand that carried French sailing culture across oceans.

Nearly fifty years on, Fountaine Pajot still feels like that original workshop: entrepreneurial, independent, family-run. But the scale has changed. Listed on Euronext Paris under the ticker ALFPC, the company is now a €200 million microcap and one of the world’s leading multihull builders. It generates steady cash, remains tightly owner-operated, and through its ODSea Lab initiative is pushing into marine electrification and vertical integration.

Where the market often sees a cyclical boatmaker, we see something different: a design-driven, vertically integrated platform with the potential to become the Rivian of the sea.

Below, we lay out the investment case for Fountaine Pajot.

Variant View: Seeing the Moat Before the Market Does

Where the market sees a French boatbuilder in a cyclical niche, navigating tariff noise and post-COVID normalization, we see a disciplined, family-run business positioning itself for the next decade. Fountaine Pajot has weathered cycles before, and while short-term sales may soften, its reinvestment in new models, careful capital allocation, and ODSea Lab electrification program point to a company steadily strengthening its hand. In a fragmented global industry, that combination of owner-operator culture and vertical integration is quietly building a moat before the market recognises it.

Final Word

Fountaine Pajot is not without risk. Leisure boats remain discretionary, and tariffs, FX swings, or a global slowdown could dent demand. But with robust free cash flow, deep insider alignment, and a measured long-term vision, the downside looks contained. The opportunity, meanwhile, is understated: the brands that will win the next cycle are those able to electrify, verticalise, and globalise. Fountaine Pajot is taking each of those steps—quietly, deliberately, and with a time horizon that extends beyond the storm.

Disclaimer:

The content published on this site is for informational and discussion purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities. The author may hold positions in the securities or companies discussed and may change these positions at any time without notice. All views expressed are personal opinions and should not be relied upon for investment decisions. Do your own research.

Culture

Fountaine Pajot is led by Nicolas Gardies, a measured operator with 21 years at the company, supported by a highly aligned leadership team that includes Romain Motteau and Mathieu Fountaine — ensuring deep ties to the founding family. Insider ownership stands at 54%, concentrated in the hands of family members and long-serving employees.

From peer, ex-employee, and industry feedback, the culture is long-term, pragmatic, low-ego, and quality-obsessed. There is no appetite for vanity growth or stock price theatrics — only consistent execution and incremental improvement.

From its humble origins with just four staff, Fountaine Pajot has grown into a dedicated team of 800+ highly skilled collaborators operating across three specialised production sites: Aigrefeuille – Core range sailing catamarans; Port Neuf, La Rochelle – Flagship catamarans, built with direct-launch capability, avoiding road transport; and Gujan-Mestras – Motor yachts production.

This blend of deep insider alignment, generational continuity, and distributed manufacturing capability underpins a culture built for endurance, not flash.

Strategic Positioning

Over the past five years, Fountaine Pajot has made a series of deliberate strategic moves that reveal an ambition far greater than first impressions might suggest. The company has diversified its offering both within the catamaran segment and beyond — most notably through the acquisition of Dufour — with a targeted focus on higher-value, premium segments. Its rebrand positions the company more firmly in the luxury space, framing its products as timeless, crafted, and artisanal — evoking the heritage of Swiss watchmaking or French luxury goods. At the same time, Fountaine Pajot has doubled down on its market-leading stance in electrification and taken greater control of its value chain, moving upstream via acquisitions of key sales distributors and downstream through the purchase of its interior manufacturing partner.

Electrifying the Blue Economy

Marine electrification remains technically complex. Boats are weight-sensitive, require long range, and operate in harsh, variable environments—factors that make battery integration and hybrid propulsion less straightforward than in cars. Today, most leading yacht manufacturers—especially in the superyacht category—offer hybrid or electric models, including Sanlorenzo, Azimut-Benetti, and Silent Yachts. In the catamaran space, players like Catana and Groupe Bénéteau (through its Excess and Lagoon brands) have also introduced hybrid-ready vessels, often in collaboration with third-party propulsion suppliers.

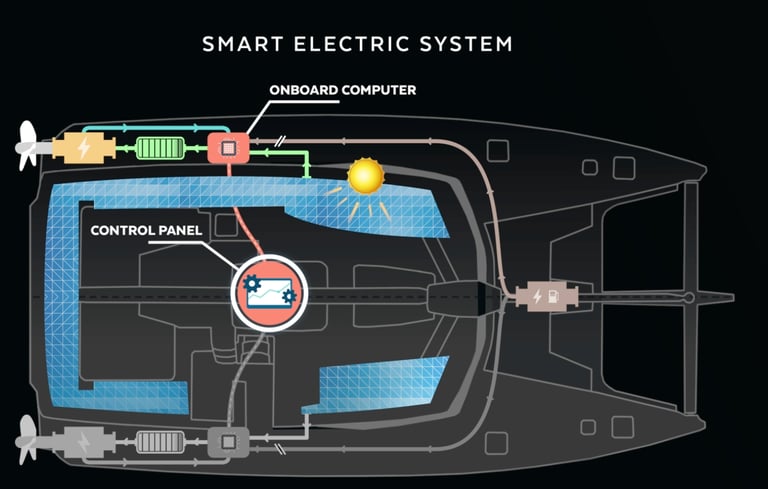

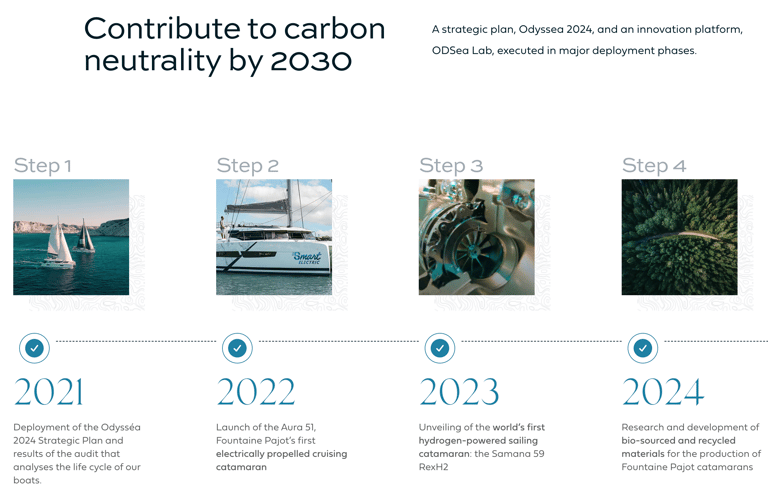

Fountaine Pajot is pursuing a more integrated approach. Through its ODSea+ initiative and the 2022 acquisition of Alternative Energies, the company has brought key electrification capabilities—solar, battery, and propulsion system design—in-house. Since 2021, it has introduced over 30 hybrid or electric boats, including models featuring 2.3kW solar arrays and a proprietary 25kW hybrid system developed by its ODSea Lab.

Fountaine Pajot’s Aura 51 Smart Electric model is already in series production, and the Samana 59 Smart Electric REXH2 prototype pushes further—integrating hydrogen-powered, zero-emission propulsion via the REXH2 fuel cell system that harnesses solar, lithium battery storage, and hydrogen to deliver extended autonomy at sea . Through ODSeaLab, and with over 60 engineers collaborating under the Odysséa 2024 strategy, the company is embedding sustainability right at the core of design, production, and lifecycle—from energy innovation to zero-carbon operation.

While Fountaine Pajot is not alone in electrification, its decision to control more of the value chain—rather than relying solely on outside vendors—suggests a longer-term commitment to building differentiated systems and product platforms across its multihull range.

Valuation

Despite its progress, we believe Fountaine Pajot remains deeply undervalued.

At the end of FY2024 the company had €66 million of net free cash on the balance sheet. With ~€20 million earmarked for new model development, that still leaves ~€46 million available for distribution over time.

Enterprise Value (normalised):

Market Cap: ~€180m

Cash: €66m

LT Debt: €25m

EV: ~€139m

Profitability & Multiples (TTM):

NOPAT: €33m

EV/NOPAT: ~4x

EV/Sales: <0.4x

P/E: <6x

Stormy Seas

Recent results from superyacht manufacturers Sanlorenzo and The Italian Sea Group, and comparative peers Lagoon-owner Groupe Beneteau and Bali-owner Catana Group, paint a mixed picture of current market conditions. There is no doubt that the volatility induced by Trump’s tariff war—layered on top of the natural reversion post-COVID—has led to a drop in demand across vessel classes.

However, the evidence suggests this is a normalization, not a collapse. Order books at Sanlorenzo and Ferretti still stretch years into the future, underscoring resilience at the ultra-high-net-worth end. Beneteau, despite sharp revenue declines, has maintained a fortress net cash position above €250 million and is launching 20 new models into the autumn shows. Catana has adjusted pricing to sustain volumes, while Sanlorenzo continues to grow revenues and backlog coverage even in a softer environment.

Against this backdrop, Fountaine Pajot stands out. Unlike peers that rely heavily on charter fleets or price discounting, FP enters this down-cycle with record profitability, a net cash fortress, and an owner-operator culture that has historically avoided chasing volume at the expense of margins. Its ODSea Lab electrification program and push into larger, higher-margin multihulls position it closer to the Sanlorenzo playbook than to mass-market peers. Yet at ~4x EV/NOPAT that disconnect is precisely where the opportunity lies.

Risks

The key (short term) downside risks are:

A prolonged post-COVID demand correction

Tariff exposure

Pullback in discretionary yacht spending by HNWIs

The Opportunity

Fountaine Pajot designs and manufactures luxury catamarans and monohull yachts under two brands: its eponymous multihull line and Dufour Yachts, acquired in 2018. The group has launched more than 4,000 vessels globally. Its boats are not built for speed alone, but for autonomy, elegance, and increasingly, sustainability.

Over the last four years, [mention the original Odyssey plan of action] the company has doubled revenues from €172 million in 2020 to €351 million in 2024. This growth has come without dilution, driven instead by careful reinvestment and disciplined capital allocation. Customers span the globe—Europe (~50%), North America (~30%), and Asia-Pacific (~20%)—and a growing percentage are shifting away from traditional diesel propulsion.

Globally, catamaran sales have grown at a compound annual rate of over 7% since 2019, outpacing monohull yacht demand—especially in the 40–60 foot leisure segment . Their appeal is no mystery: catamarans offer greater stability, wider deck space, and shallower draft, making them ideal for family cruising, charter use, and newer sailors seeking comfort and safety over raw speed. The twin-hull design reduces heel and motion at sea, improving both fuel efficiency and onboard liveability. As post-COVID boating demand persists and sustainability rises on the agenda, catamarans are increasingly viewed as the modern sailor’s vessel of choice—combining luxury, function, and versatility in one elegant frame.

Catamarans have long been favoured in Europe and the Caribbean but they remain relatively under-penetrated in the U.S. leisure boating market. While the U.S. accounts for nearly half of the global recreational boating industry by revenue, multihulls represent a small fraction of domestic registrations compared to their dominance in European and charter markets. This is surprising, especially considering the catamaran’s natural advantages for American coastal and harbour cruising and exploring inlets, bays, and intracoastal waterways for the reasons outlined above (shallow draft and maneuverability) . They're also increasingly popular among anglers and day cruisers seeking more deck space, fuel efficiency, and stability than a traditional monohull.

ODYSSEA 2028: A Blueprint for Growth

Looking ahead, Fountaine Pajot has laid out a clear five-year roadmap. Under its ODYSSEA 2028 plan, the group will launch 11 new models (6 catamarans, 5 monohulls), continue its electrification push, and invest €19 million into modernising production.

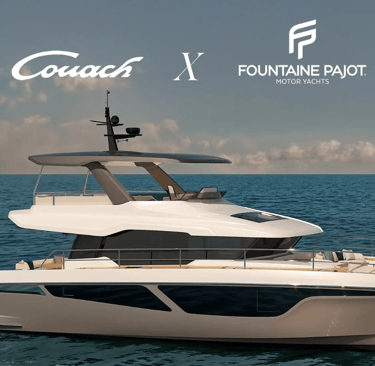

A particularly strategic product is the upcoming Code 07—a 50-foot motor yacht designed specifically for U.S. buyers. Developed under the Veya brand—a joint venture between Fountaine Pajot and French builder Couach Yachts—the Code 07 represents Fountaine Pajot’s boldest effort yet to enter the U.S. power yacht market.

This JV is being led by Romain Motteau, the company’s Deputy Managing Director, signaling the seriousness of the initiative. If successful, it could unlock a large, brand-loyal customer base—and expand margins beyond the European sailing crowd.

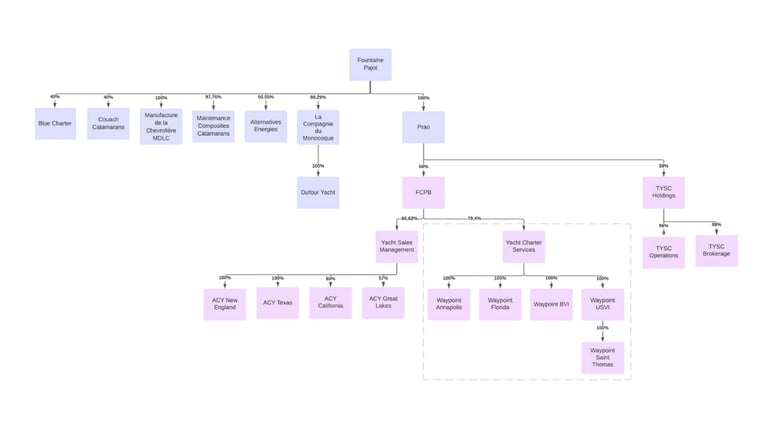

Vertical Integration: Owning the Journey

But electrification is only one part of the transformation. The company is bringing the value chain in-house. To reduce dependency on suppliers and elevate the brand experience, Fountaine Pajot has been following the lead of listed superyacht peers SanLorenzo and The Italian Sea Group by vertically integrating both its supply chain and sales funnel:

In 2024, it acquired Malvaux Industries’ 8,000 m² outfitting plant in La Chevrolière, giving it greater control over cabinetry, interiors, and finishings.

In the same year, it took a controlling stake in The Yacht Sales Co., a premier distributor in Asia-Pacific with presence in 11 countries—boosting both sales reach and customer service. This follows on from the 25% stake it acquired in Atlantic Cruising Yacht, a US based distributor, in 2023.

In 2022, it acquired Alternative Energies, bringing electric propulsion and hybrid R&D into the group.

This approach mirrors the best compounders in other industries: control the brand, own the engineering, deepen customer relationships, and scale quality.

Copyright Komorebi Investments Pty Ltd 2025